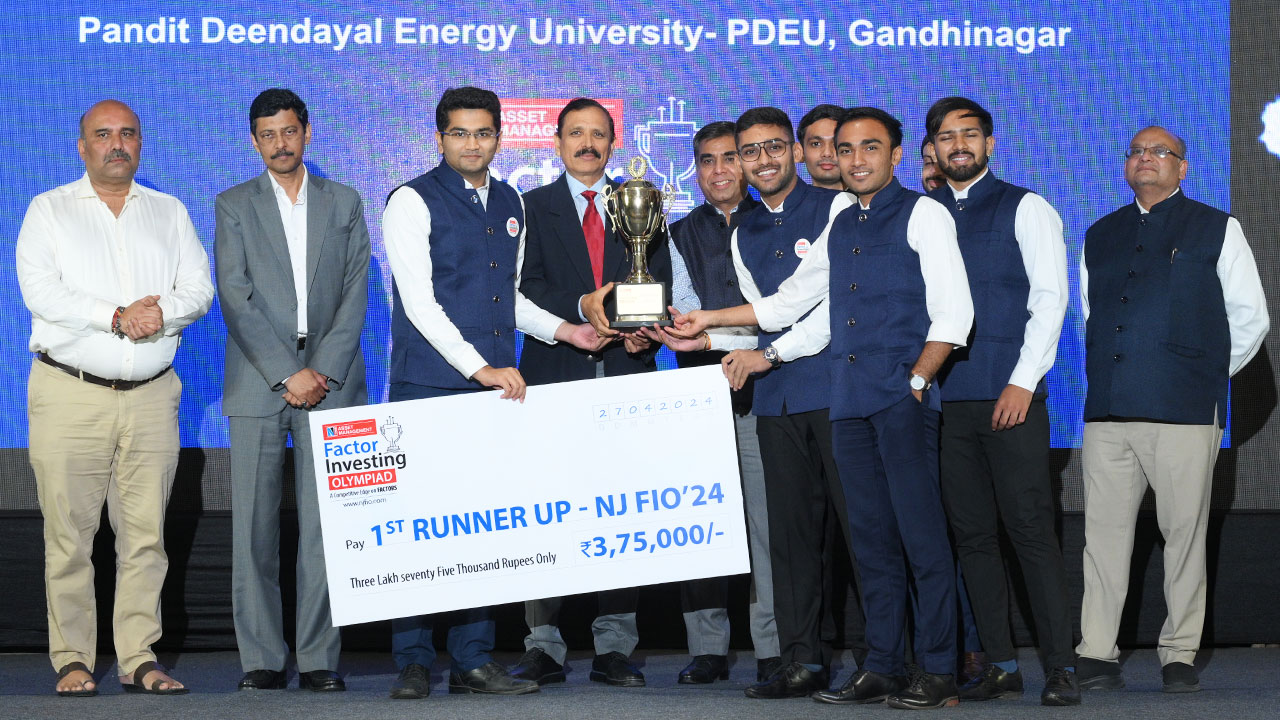

An Annual Competition in Factor Investing for India's Top B-Schools.

Unique platform for students from India's premier business schools.

Tackle real-world challenges encountered by investment managers.

Annual competition rooted in the principles of factor investing.

Participating teams can showcase their analytical and strategic skills.

Unique knowledge initiative to spread awareness about rule-based and factor investing.

Strong emphasis on education and empowerment.

Nurture the next generation of informed investors.

Reflection of NJ AMC's broader commitment to responsible investing and knowledge-sharing.

Driven by the belief that spreading financial literacy is a shared societal responsibility.